According to General Administration of Customs data, China’s foreign trade grew by 4.8 percent on a yearly basis to 9.89 trillion yuan (USD 1.44 trillion) in the first quarter of 2023.

The data shows the country’s exports rose 8.4 percent year-on-year to RMB 5.65 trillion yuan, while imports rose by a modest 0.2 percent to RMB 4.24 trillion.

Trade with ASEAN, its largest trading partner, was a major driver reaching RMB 1.56 trillion in the first quarter, up 16.1 percent, accounting for 15.8 percent of China’s total foreign trade.

Imports and exports to the European Union, the United States, Japan and the Republic of Korea reached RMB 1.34 trillion, RMB 1.11 trillion, RMB 546.41 billion and 528.46 billion, respectively, over the same period, accounting for 35.6 percent of the country’s foreign trade.

From January to March, China’s imports and exports with economies participating in the Belt and Road Initiative surged 16.8 percent year-on-year accounting for 34.6 percent of its foreign trade, while trade with other participating countries of the Regional Comprehensive Economic Partnership rose 7.3 percent from the first quarter of 2022.

A version of this article originally appeared in Beijing Review.

With the U.S. economy still reeling from the COVID-19 pandemic and record unemployment, real estate prices continue to skyrocket pricing thousands of house hunters out of the market in the U.S. and Canada. This may seem counterintuitive for an economy that has technically been in recession since February 2020 and saw unemployment peak at just over 14% last April. The last time U.S. home prices raised this quickly, it led to an ensuing crash that brought down the global economy.

This asset bubble is not restricted to the US but is crossing borders and going global making housing or even renting unaffordable for many – especially those worst affected by the global pandemic. In fact the rate of price increases has alarmed policy makers in both the U.S. and Canada. “The dream of homeownership is out of reach for so many working people,” Senate Banking Chair Sherrod Brown told Politico recently. “Rising home prices and flat wages means that many families, especially families of color, may never be able to afford their first home.”

According to World Population Review “the typical value of U.S. homes was $269,039 as of January 2021, a 9.1 percent increase from January 2020. Between 1999 and 2021, the median price has more than doubled from $111,000 to $269,039.

Canadian Prime Minister, Justin Trudeau has also weighed into the topic recently in a statement saying that the cost of owning a home is too far out of reach for too many people in Canada’s largest cities, noting it can take 280 months for an average family to save for a down payment in a place like Toronto or Vancouver – a favorite with Chinese migrants.

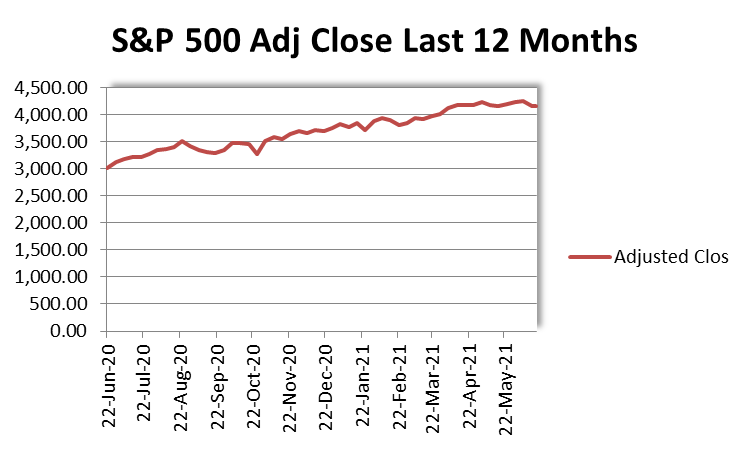

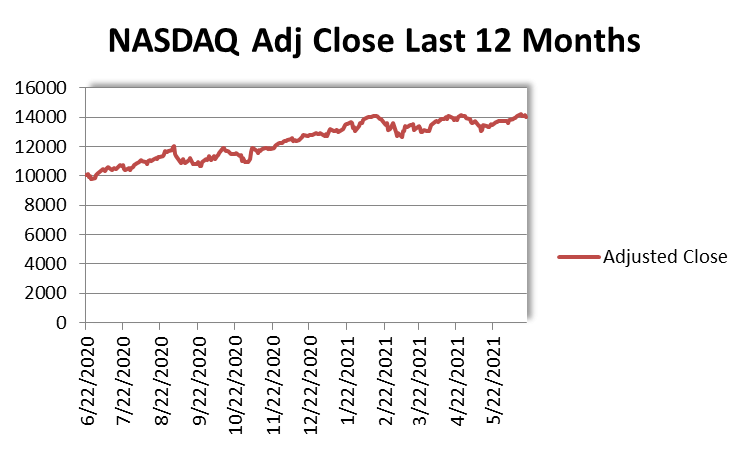

But real estate is not the only asset class that is being inflated; both the NASDAQ and S&P 500 have increased by nearly 40% in the last 12 months despite unemployment near record COVID highs in the U.S. The NASDAC increased by 39.51% in the last 12 months while the S&P 500 rose 38.46% over the same period.

Source: Yahoo FinanceSource: Yahoo Finance

The source of this asset bubble inflation is the Federal Reserve’s policy of Quantitative Easing or QE – a term economist use to describe printing money and using it to buy back domestic treasury bonds from banks and other financial institutions. This, in theory, is designed to reduce the interest rate and encourage lenders to lend to industry or individuals to stimulate the ‘real’ or productive economy.

In reality, much of this ‘free money,’ as Professor Michael Hudson, financial analyst and president of the Institute for the Study of Long-Term Economic Trends, contends is instead used to speculate on assets both domestic and international – particularly in emerging markets where the biggest and quickest gains can be made. In essence, QE disproportionately benefits those closest to the Fed. These asset bubbles show no sign of abating as the US is expected to approve an addition 2 trillion in stimulus this year and the Fed has said it won’t take it’s foot off the pedal when comes to pumping liquidity into the market.

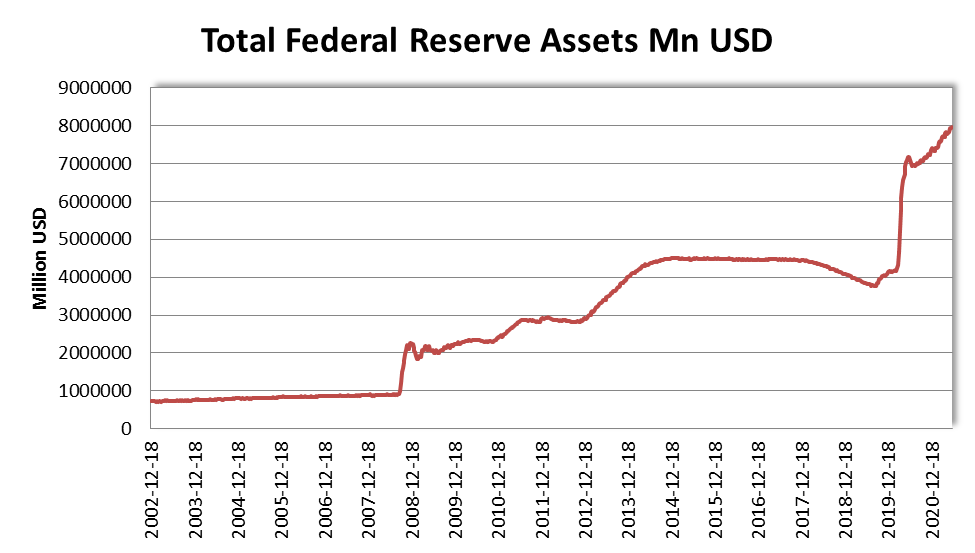

Source: FRED The chart above shows the growth of money supply from the Federal Reserve since 2002. Note the volume doubled during the Financial Crisis of 2008. From then on the economy continued to be buoyed up with periodic bouts of money printing before rocketing during the 2020 COVID-19 pandemic.

With many of these dollars being spent abroad the central banks of the receiving countries keep them and pay the receiver in local currency. But what can central banks around the world do with all these dollars.

As congress often blocks attempts to purchase U.S. companies and assets under the guise of national security – as with the Chinese oil company CNOOC’s $18.5 billion bid for Unocal in 2005 – there is only really one option left; to purchase U.S. Treasury Bonds or T-bills to further underwrite U.S. debt. All of this is made possible because of the U.S. dollar’s unique status as the world’s reserve currency.

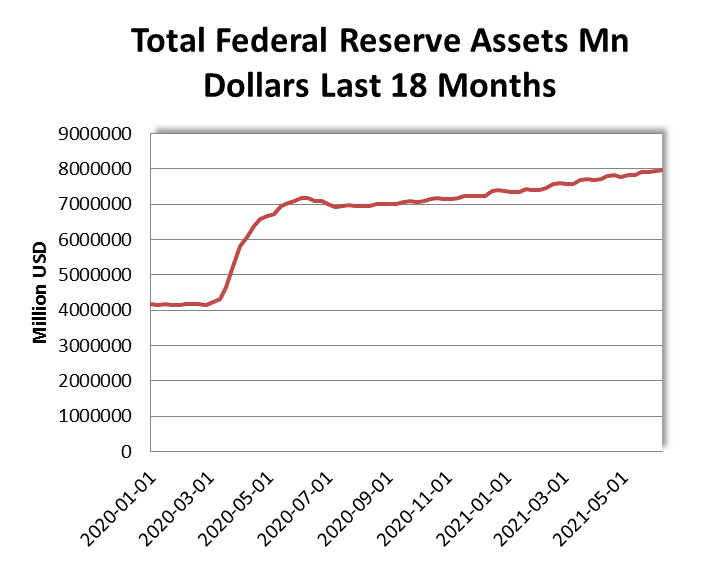

Source: FRED The graph shows how Federal Reserve money supply has nearly doubled in the last 18 months.

Aside from printing money ad infinitum, this special status as global reserve currency gives the U.S. another ability. Namely, to sanction countries or individuals that do not align with their foreign policy objectives. Potentially, it gives the U.S. the ability to essentially turn off the economies of counties that don’t follow U.S. hegemony for whatever reason. But it is this threat and the increasingly liberal use of unilateral sanctions that are leading some economies to attempt to de-dollarize their economies and insulate them from economic bullying.

One such country is Russia. On June 3, the Kremlin announced its policy outline for de-dollarization. The plan to abandon the US dollar was developed by the government in response to tougher US sanctions. Finance Minister Anton Siluanov announced plans to reduce the share of the dollar in the Russian National Wealth Fund (NWF) to zero.

“I can only say that the de-dollarization process is constant,” said Siluanov, expressing doubts about the reliability of the main reserve currency, at a press conference at the St. Petersburg International Economic Forum. According to him, this process is taking place not only in Russia, but also in many countries. “We made a decision to withdraw from dollar assets completely, replacing them with an increase in euros, gold, and other currencies,” the minister said.

According to him, as the share of the dollar is reduced to zero, the share of the euro will be 40%, the yuan 30%, gold 20%, pounds and yen 5% each. Siluanov, noted the replacement will take place “rather quickly, perhaps within the month”. Even before the Ministry of Finance announcement, the Bank of Russia carried out a large-scale restructuring of its gold and foreign exchange reserves, shifting about $100 billion in 2018 into euros, yuan and yen.

Added to this, at the end of 2019, several European countries set up a new transaction channel designed to facilitate companies to continuing to trading with Iran despite US sanctions after President Donald Trump unilaterally withdrew from the nuclear agreement or the Joint Comprehensive Plan of Action (JCPOA).

Set up by Germany, France and the UK, the ‘Instrument in Support of Trade Exchanges’ or INSTEX gives European companies the capacity to bypass the U.S. controlled SWIFT banking system – a network that enables financial institutions worldwide to send and receive information about financial transactions and one of the main tools for U.S. sanctions.

“We’re making clear that we didn’t just talk about keeping the nuclear deal with Iran alive, but now we’re creating a possibility to conduct business transactions,” German Foreign Minister Heiko Maas told reporters at the time.

In addition, China launched its Cross-border Interbank Payment System (CISP) in 2015. CISP is a payment system which offers clearing and settlement services for participants in cross-border yuan payments and trade.

At the start of the 21st Century the idea of de-dollarizing global trade seemed insurmountable. But now it seems as if the COVID-19 pandemic and America’s response may be accelerating the process faster than many imagined possible.

China commodity prices for such materials as iron ore, steel rebar, coal and copper soared to record highs in May forcing the government to intervene and curb cost increases for consumers.

As the world’s largest manufacturer and construction market, China has been the main driver behind global metal markets for more than a decade.

From January to mid-May, prices for steel rebar, hot-rolled steel coil and copper rose more than 30% as construction and manufacturing expanded in the world’s largest consumer of metal.

Other vital industrial inputs including iron ore, thermal coal, sulphuric acid and glass also roser to record highs as consumption outpaced supply.

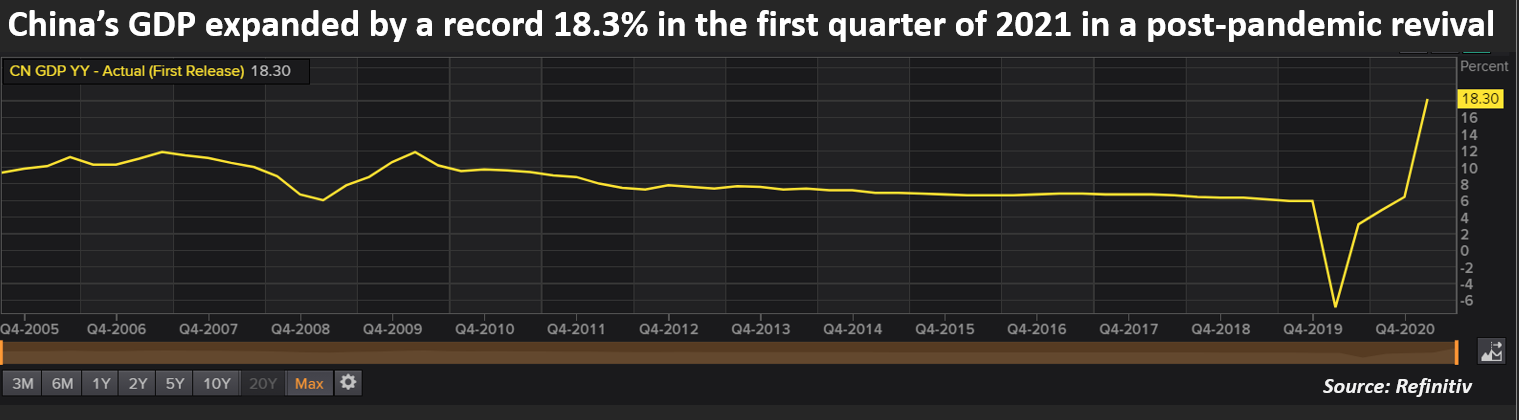

China’s economic recovery accelerated sharply in the first quarter of 2021 after the coronavirus lull in 2020

The huge government stimulus measures launched at the height of the COVID-19 lock-down last year spurred construction activity, while the world’s largest manufacturing base capitalised on booming demand for appliances, exercise equipment and machinery in locked-down countries around the world from mid-2020.

With rising raw material prices stoking fears of inflation, the government is urging coal producers to boost output while investigate behaviour that may be bidding up prices.

Regulators in Shanghai and the steel hub of Tangshan warned mills this month against price gouging, collusion and irregularities, and said they would close businesses of those disrupting market order.

China’s commodity price rises have been further exacerbated by global shipping rates. The Baltic Dry Index (BDI) – a bell weather for dry freight rates – surged to a 19-month high underpinned by excess demand and COVID affected supply.

Since the turn of the 21st Century, China’s State Owned Enterprises (SOEs) have undergone a dramatic transformation that is widely misunderstood. Since China joined the World Trade Organization (WTO), its trade surplus has ballooned and SOE share of total exports as dropped relative to private enterprise to become relatively small. To many, this shift is correlated with moves in the late 1990s to ‘reign in’ SOEs and restructure the economy along market lines. However, the real picture is more complicated and far more interesting than this common-sense conclusion. In fact, almost all of the 57 Chinese firms on the Fortune Global 500 list are SOEs.

This phenomenon is puzzling to those who would naturally assume that relatively inefficient SOEs should be out-competed by more efficient private enterprises in a market environment. To understand this paradox, it is important to understand the nature of the shift that occurred at the end of the 1990s.

At the time, Western government’s around the world assumed that Zhu Rongji’s efforts to reform the SOE sector was akin to Gorbachev’s Perestroika program. When in reality the goal was to move toward a much more sophisticated model.

While thousands of workers were let go and vast sprawling heavy industry plants cut loose, something else was also happening. SOE enterprises were quietly repositioning themselves away from highly competitive, export-oriented, downstream industries and consolidating their grasp over lower competition, highly monopolistic up-stream industries – for example, telecommunications, information transfer, storage, banking, energy, transport and post.

At the same time, this freed privately owned, competitive enterprises to concentrate on lower value, more volatile, export-orient industries. This restructuring also drastically increased demand for the intermediate goods, services and factors SOEs provide allowing them to charge monopoly prices consolidating the party’s control over the economy at large.

With SOE enterprises ostensibly under government control, instead of freeing the economy from SOEs, this upstream/down-stream restructuring created a hyper-profitable SOE sector capable of subordinating the private economy into lower value markets, consolidating State control over the economy at large.