As countries around the world contend with the health emergency of the COVID-19 pandemic, the economic effects of mitigation measures have immediately impacted the world’s commodity markets and are likely to continue to affect them in the longer term.

The global economic shock of the pandemic has driven most commodity prices down and is expected to result in substantially lower prices over 2020, the April Commodity Markets Outlook reports. The following figures are courtesy of the World Bank.

The COVID-19 pandemic is expected to plunge most countries into recession in 2020, with per capita income contracting in the largest fraction of countries globally since 1870. Advanced economies are projected to shrink 7 percent. That weakness will spill over to the outlook for emerging markets and developing economies, who are forecast to contract by 2.5 percent as they cope with their own domestic outbreaks of the virus.

Taking care of the land and preserving biodiversity – through healthy soil, reliable water access and pollinators – is vital for providing livelihoods for rural populations, particularly during times of economic shock like that caused by the current COVID-19 pandemic.

Healthy ecosystems have been shown to provide a lifeline to the poorest. The Poverty Environment Network project that collects income data of forest adjacent communities from 24 countries, estimates that environmental income (most of it from the forest) represents 28 percent of total income of these households

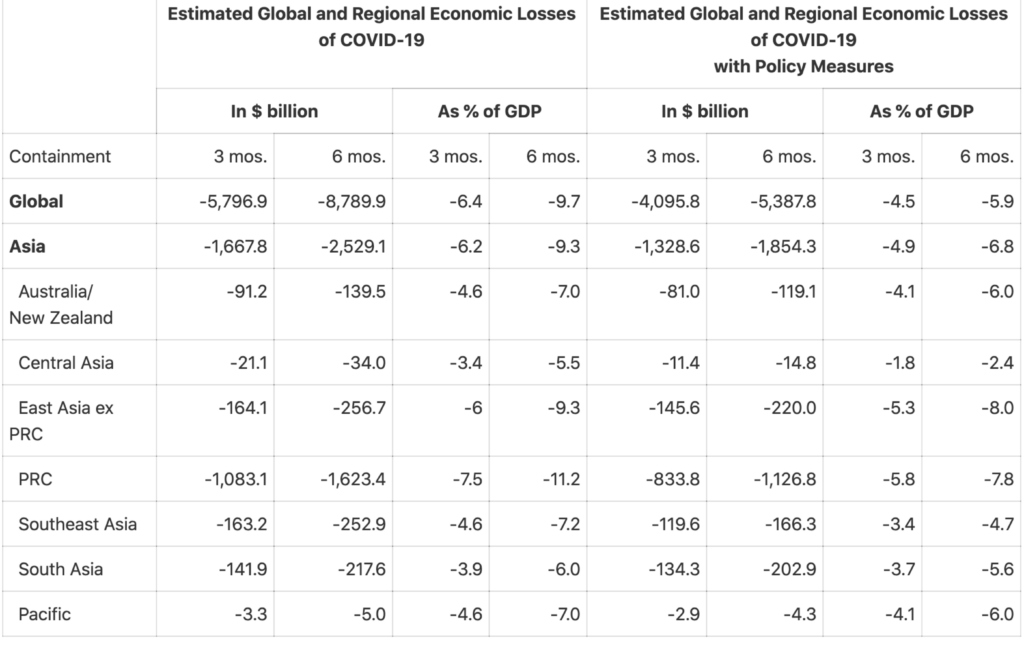

According to the Asian Development Bank the global economy could suffer between USD5.8 trillion and USD8.8 trillion in losses—equivalent to 6.4% to 9.7% of global gross domestic product (GDP)—as a result of the Corona Virus pandemic.

The report finds that economic losses in Asia and the Pacific could range from USD1.7 trillion under a short containment scenario of 3 months to USD2.5 trillion under a long containment scenario of 6 months, with the region accounting for about 30% of the overall decline in global output. The People’s Republic of China (PRC) could suffer losses between USD1.1 trillion and USD1.6 trillion.

Governments around the world have been quick in responding to the impacts of the pandemic, implementing measures such as fiscal and monetary easing, increased health spending, and direct support to cover losses in incomes and revenues. Sustained efforts from governments focused on these measures could soften COVID‑19’s economic impact by as much as 30% to 40%, according to the report. This could reduce global economic losses due to the pandemic to between $4.1 trillion and $5.4 trillion.

The analysis, which uses a Global Trade Analysis Project-computable general equilibrium model, covers 96 outbreak-affected economies with over 4 million COVID-19 cases. In addition to shocks to tourism, consumption, investment, and trade and production linkages covered in the ADO 2020 estimates, the new report includes transmission channels such as the increase in trade costs affecting mobility, tourism, and other industries; supply-side disruptions that adversely affect output and investment; and government policy responses that mitigate the effects of COVID-19’s global economic impact.

Under the short and long containment scenarios, the report notes that border closures, travel restrictions, and lockdowns that outbreak-affected economies implemented to arrest the spread of COVID-19 will likely cut global trade by $1.7 trillion to $2.6 trillion. Global employment decline will be between 158 million and 242 million jobs, with Asia and the Pacific comprising 70% of total employment losses. Labor income around the world will decline by $1.2 trillion to $1.8 trillion—30% of which will be felt by economies in the region, or between $359 billion and $550 billion.

Source: ADB staff estimates.

Note: The 3-month and 6-month containment periods assumed in the scenarios are country-specific. They are the assumed time needed for a country to get a domestic outbreak under control from when the outbreak intensifies and start normalizing economic activity.

Apart from increasing health spending and strengthening health systems, strong income and employment protection are essential to avoid a more difficult and prolonged economic recovery. Governments should manage supply chain disruptions; support and deepen e-commerce and logistics for the delivery of goods and services; and fund temporary social protection measures, unemployment subsidies, and the distribution of essential commodities—particularly food—to prevent sharper falls in consumption, the report says.

Caixin is reporting that China has suspended debt repayments for 77 developing countries and regions as part of the G-20 debt relief initiative to help impoverished countries weather economic difficulties amid the coronavirus pandemic, a senior Chinese diplomat said on Sunday.

The measures were announced by Chinese Vice Foreign Minister Ma Zhaoxu in Beijing.

Ma offered no details nor beneficiaries, the amount involved or terms of repayment.

The announcement came after G-20 agreed in April to freeze debt service payments until the end of the year for the world’s poorest countries battling Covid-19.

In May, President Xi Jinping also pledged $2 billion in aid and donations over the next two years to relevant countries and organizations combatting the pandemic.

According to the vice foreign minister the pledged aid included a USD50 million donation to the World Health Organization (WHO).

Wang Zhigang, minister of science and technology, also said during the same press conference that China will make its Covid-19 vaccine “a global public good” when it is ready.

China’s top epidemiologist Zhong Nanshan said on Saturday during a livestreaming event that he believed the long-awaited coronavirus vaccine could be available for emergency use as early as this fall or by the end of the year. In total, six candidate vaccines are undergoing clinical trials in China.

Lao-China Railway Could boost aggregate income by 21% according a recently released World Bank report. Part of China’s grand Belt and Road Initiative(BRI), the railway connecting Lao and later Thailand, Malaysia and Singapore to the ambitious BRI if the right reforms are undertaken by the Lao Government.

The 414km long stretch of the high-speed rail-network connecting the capital, Vientianeand Boten at the border with China could provide Lao with a land link to global and regional supply chains – making the country more attractive to investors and hence growth.

But for this to happen, the government is faced undertaking bold, and sweeping policy reforms to facilitate trade, improve connectivity and simplify rules around doing business. These reforms would make the country attractive as an investment destination and link it to major production and consumption bases – like China and the Association of South East Asian Nations (ASEAN) – allowing firms to access global value chains.

The report goes on to say that “With efficient logistics services, Lao PDR could develop into a logistics hub, while targeted investments in agriculture and tourism could result in new export opportunities.”

At present, the production costs of USD5.9bn (a bit more than a third of Lao’ GDP) are to be shared 30/70 with China paying the lion’s share. But the high costs presents major risks for a country as economically challenged as Laos.

Forty percent of construction will be funded through equity, with one-third provided by the Lao Government (partially funded through loans from the Export-Import Bank of China) and the remaining two-thirds funded by China. This 60 percent will be funded by loans from the Lao-China Railway Company, a State- Owned Enterprise with 30 percent Lao and 70 percent Chinese ownership.

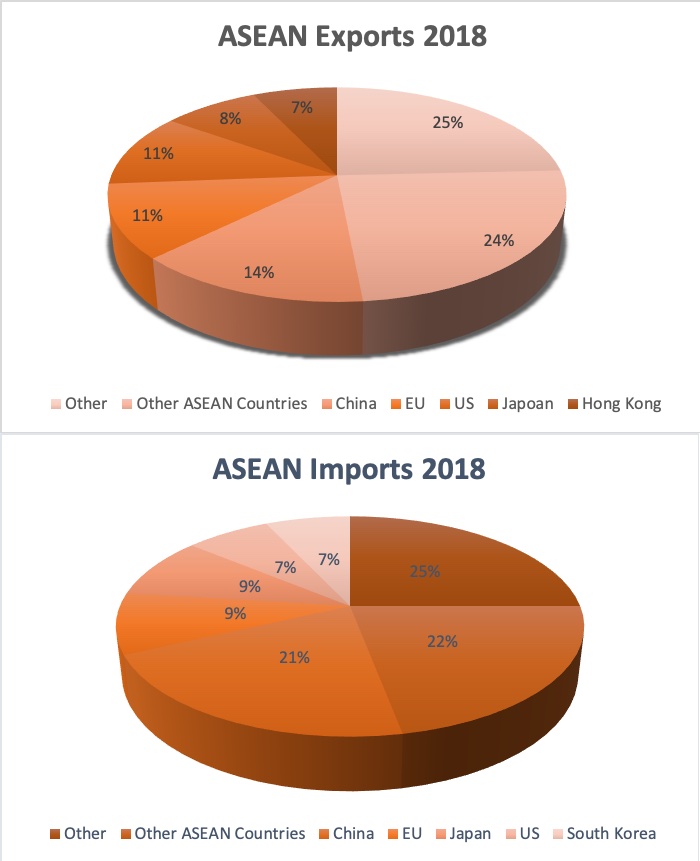

Success of the project will depend on China switching it’s current maritime cargo strategy to SE Asia and moving to rail. Most cargo destined for SE Asia is shipped and trade between China and Lao represents less than 2% of all China-ASEAN trades.

In 2019, China’s trade volume with ASEAN climbed by 14 percent to 4.43 trillion yuan. The EU remained China’s single largest trading partner with 4.86 trillion yuan in bilateral trade and an eight percent year-on-year growth rate (the U.S. has relegated to the third place on the list of China’s top trading partners with bilateral trade contracting more than 10 percent to around 3.73 trillion yuan).

(Source Eurostat)

The report estimates transit trade through the Laos railway corridor could reach an estimated 3.9 million tonnes per year by 2030, given a shift of 1.5m tonnes from the maritime transport sector.

Lao’s tourism industry could benefit greatly from an increase in demand for passenger rail traffic, which is expected to account for the majority of train traffic by 2030.

If Lao implements necessary logistics and trade reforms, the railway could attract traffic that is currently using maritime and air transport routes and significantly reduce land transport prices by 40-50 percent between Vientiane and Kunming, China and by 32 percent between Kunming and the Port of Laem Chabang in Thailand once the Lao-China railway starts to operate in December 2021.

Amid the talk of a new Cold War with China some analysts are warning that China could use weaponize its vast foreign currency reserves – it’s massive US Treasury Bond Holdings (T-Bills) – and dump them on the open market. To understand this arrangement read Understanding China Foreign Exchange.

Often referred to as the ‘nuclear option,’ – and not without good reason – has the potential to cause a massive spike in U.S. interest rates, sink the US stock market and freeze credit markets, pushing the U.S. even further and deeper into recession. This would of course create major problems for whoever happens to be President.

The problem is, for the alarmists, they underestimate the damage this do to the Chinese economy. Firstly the as the selloff started the overall value of it’s holdings would plummet; meaning China would be getting pennies on the dollar for what it has taken years to save.

A second factor is that such a move would push Beijing’s dream of the RMB as a reserve currency – a hard policy objective for many years – decades into the future. It would also leave the US relatively unscathed in the short term as the Fed – as it loves to do – could simply print the money to buy back the Treasury Bonds, in a kind of Buzz Lightyear QE ‘To Infinity and Beyond’ program. The economic equivalent of kicking the financial can another generation or two down the road.

China is now world’s second largest importer

It would also terrify foreign investors in China as the value of the RMB lost stability. One of the ways Beijing controls the value of the RMB is by maintaining a foreign currency reserve basket – of which, at present T-Bills make up about USD1.1 trillion as of March 31, 2020. The majority of which are held as reserves to collateralize trade and to capitalize China’s banking system.

Furthermore, a mass selloff would put downward pressure on the RMB and force China to devalue it’s currency and continuing the selloff could lead to a depreciation spiral. A spiral that would make it ever harder to retrieve those dollar reserves.

This spiral would have been less of a worry twenty years ago when China could claw back dollars hand over fist with its epic trade surplus. But those days are long gone, and trade surpluses in the future are likely to be far more meagre, especially as China enters uncertain economic territory as the global Covid-19 crisis continues to wreak economic havoc around the world.

This combination of factors ensures China will continue to need substantial foreign currency reserves both to maintain it’s exchange rate against hard currencies but also to ensure it retains it’s capacity to settle hard currency denominated trade – especially important now China is the world’s second largest importer.

But let’s not get complacent. While the ‘nuclear option’ may be off the table, Beijing has many more weapons in it’s arsenal it could use to make more than uncomfortable for the US. An embargo on rare earth minerals would be one.