Fixed Asset Investment (FAI), a measure of capital spending on physical assets (real estate, infrastructure, machinery, etc.), remains a cornerstone of China’s economic model. Compiled by the National Bureau of Statistics (NBS), FAI data is published monthly, quarterly, and annually, with breakdowns by sector and ownership type (SOEs, private firms). Projects exceeding 5 million yuan are included, with SOEs reporting directly and smaller projects aggregated regionally. Sector-specific investments (e.g., railways, highways) are reported by relevant ministries.

FAI Trends (2023–2025)

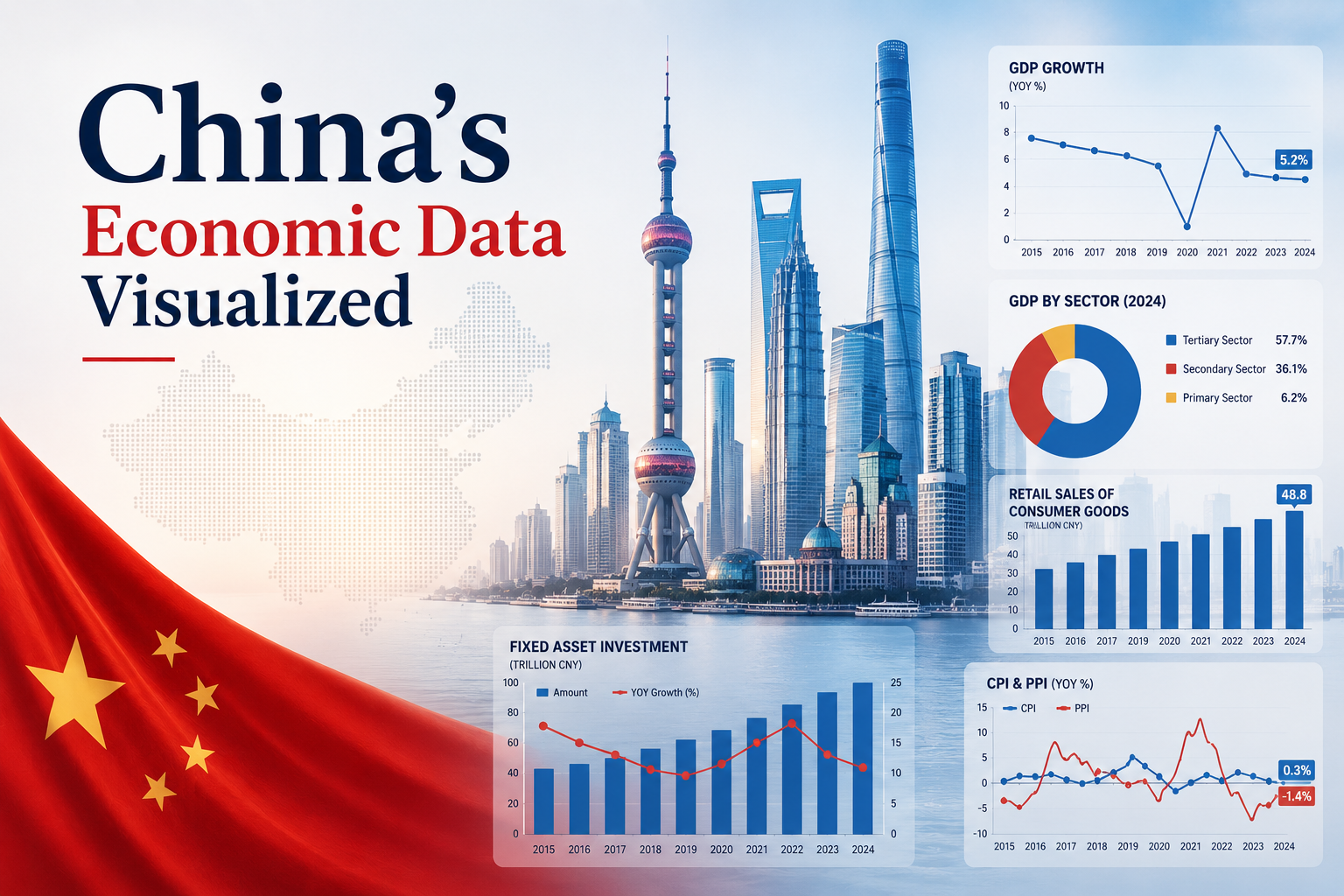

(The chart below tracks FAI growth YoY, highlighting sectoral shifts and policy impacts.)

Key 2025 Observations:

-

Slowdown Persists: FAI growth decelerated to 3.8% YoY in H1 2025 (vs. 4.5% in 2024), dragged by real estate (-2.1%) despite infrastructure stimulus (6.4%).

-

Policy Pivot: Manufacturing FAI (5.2%) reflects Beijing’s push into high-tech and EVs, while property woes deepen.

-

Seasonality: The usual Q1 surge (budget front-loading) was muted in 2025, signaling fiscal caution.

Why FAI Still Matters in 2025

-

Growth Dependency: China’s economy remains investment-driven, with FAI accounting for ~40% of GDP. Household savings (locked in state banks) fuel SOE borrowing, sustaining the cycle.

-

Debt Risks: FAI’s link to local government financing vehicles (LGFVs) and property developers amplifies systemic fragility. Ghost cities (e.g., Ordos) and vacant “bridges to nowhere” persist, with 2025’s property slump exacerbating overcapacity.

-

Global Spillovers: FAI drives demand for commodities (iron ore, copper), tying the Australian dollar and emerging-market exports to China’s investment cycles.

FAI Composition: Sectoral Breakdown (2025)

Sectoral Shifts:

-

Real Estate’s Decline: Share of FAI fell to 22% in 2025 (vs. 28% in 2020) as developers retrench.

-

Infrastructure Dominance: 32% share, fueled by “new infrastructure” (5G, data centers) and disaster-resilient projects.

-

Manufacturing Resilience: 28% share, with green tech (solar, EVs) offsetting traditional industry cuts.

Risks and Rebalancing

-

Debt Overhang: FAI’s reliance on debt (LGFV borrowings hit $9tn in 2025) threatens financial stability.

-

Deflation Threat: Overcapacity in property and steel sustains factory-gate price declines (-1.2% YoY, July 2025).

-

Policy Dilemma: Beijing faces pressure to stimulate FAI (short-term growth) or pivot to consumption (long-term rebalancing).

Bottom Line: FAI remains a vital but flawed growth lever. In 2025, its contradictions—between SOE-driven excess and high-tech ambition—mirror China’s broader economic crossroads.

Return to: China’s Macro Data Visualized

Explore: Cityscape Investment Series